-

Be sure to read this post! Beware of scammers. https://www.indianagunowners.com/threads/classifieds-new-online-payment-guidelines-rules-paypal-venmo-zelle-etc.511734/

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Stocks, Gold, Silver, and the printing press.

- Thread starter smokingman

- Start date

-

- Tags

- precious metals

The #1 community for Gun Owners in Indiana

Member Benefits:

Fewer Ads! Discuss all aspects of firearm ownership Discuss anti-gun legislation Buy, sell, and trade in the classified section Chat with Local gun shops, ranges, trainers & other businesses Discover free outdoor shooting areas View up to date on firearm-related events Share photos & video with other members ...and so much more!

Member Benefits:

$10? Good luck with that.

Time will tell, but in 6 months from now we can look back at this thread and see how it looks.

Now $16.36 per 1-oz 0.999 silver round at Provident.

I hate myself for panicking a couple of years ago and acquiring silver when it was selling for $30-45 per oz.

Damn, I wonder if you were the guy who bought most of mine? I dumped a bunch of 1oz silver for over $45/oz back then.

What would advise someone who wants insurance to do is buy a little gold all the time. We all know how a FIAT currency will end. It will be accompanied by an ever increasing government debt bubble, plunging interest rates as the government seeks to hide it's profligate ways, and eventually a hyper-inflationary death shudder wiping out paper assets then the currency.

Many people believe that gold will be the only thing people will trade goods for but that's wrong (at least in a historical sense). Many things will be bartered, including gold and silver. However the real advantage that gold will have will be as a bridge for the saved wealth from this financial system to the next system.

Gold will retain it's value, just as it has for thousands of years. think a safe T-Bond will do that? How about a CD? How about anything else that carries counter-party risk in our completely insane, fractional reserved world?

Nothing in our financial system has been fixed since little investment bank Lehman Brother went under. That little bank, and it's little bonds that other financial institutions owned was enough to take down the entire system. The reason is that these institutions operate on 2-5% equity and huge amounts of leverage. If they lose even a small amount of their reserve capital they are bankrupt (well they're bankrupt already since they cannot pay off all their creditors!) Every bank is the same way.

If someone can't pay, then nobody can pay and the mad scramble ensues to grab whatever real asset you can. If you have some gold you have a real asset that carries no counter-party risk, is portable, convertible, and durable. It also carries the premium of being the one true monetary metal. Silver has been used as money, but it's best uses are in other things. It is consumed while gold is not.

I think every should own some physical gold.

There is a little saying I heard that I think makes a whole hell of a lot of sense. In the Great Depression of the 20-30s there were all sorts of goods to be purchased but no one had any money to buy those things. (deflationary depression)

In the next Great Depression everyone will have all sorts of money, but you won't be able to buy anything with it. (inflationary depression)

We are well on our way.

Damn, I wonder if you were the guy who bought most of mine? I dumped a bunch of 1oz silver for over $45/oz back then.

If it was going through a coin shop in Lafayette on its way to me, then I might have been your huckleberry!

It was . . . a learning experience.

If it was going through a coin shop in Lafayette on its way to me, then I might have been your huckleberry!

It was . . . a learning experience.

It'll go back up.

Ultra-low interest rates, set by dictate rather than the free market, results in a net gain by debtors and a net loss by savers. Guess who the biggest debtor is. Don't worry about all those people with savings account or who buy govt securities to provide safety in their retirement. They didn't need the money anyway. source

Interest rates necessarily reflect the balance between saving/investing and borrowing/spending.

That's why it's important to view interest rates less as a thermostat and more as a thermometer.

More spending and borrowing tends to be inflationary because it increases the velocity of money. This higher inflation should raise rates, making it more appealing to be a saver and less appealing to borrow money, which tends to be deflationary and push rates back down.

If allowed to communicate effectively this economic information, interest rates help the market sort things out.

Low rates of return in investment accounts also come with low rates of inflation (generally speaking-- hence the 'mysterious anomaly' of stagflation). One need not be an investing superhero to beat the rate of inflation in your accounts.

Interest rates necessarily reflect the balance between saving/investing and borrowing/spending.

That's why it's important to view interest rates less as a thermostat and more as a thermometer.

More spending and borrowing tends to be inflationary because it increases the velocity of money. This higher inflation should raise rates, making it more appealing to be a saver and less appealing to borrow money, which tends to be deflationary and push rates back down.

If allowed to communicate effectively this economic information, interest rates help the market sort things out.

Low rates of return in investment accounts also come with low rates of inflation (generally speaking-- hence the 'mysterious anomaly' of stagflation). One need not be an investing superhero to beat the rate of inflation in your accounts.

How do interest rates reflect anything but the whim of the fed?

Gas usage in the USA for 2013 is less than 1/2 of what is was in 1980 and rapidly declining.Yes since 1980 fuel efficiency has improved 60%,however the population has gone from 226,545,805 to just over 317,00,00.

There are over 254 million licensed cars currently vs 162 million in 1980.The bottom line is less American people can afford gasoline.We are using less than 50% nationally than we have at any time since the oil crisis(anyone remember that when oil went from $3.00 a barrel to $12.00 those where the days),and the decline has been rapid and sharp since 2007.In 2007 we used an average of 59,000,000 gallons per day,today that figure is at just over 18,000,000.Also of note our number one export is refined petroleum(gas and diesel).

U.S. Total Gasoline Retail Sales by Refiners (Thousand Gallons per Day)

Chicken,meet roost.

http://www.ft.com/cms/s/0/8b33af5c-76d8-11e4-8273-00144feabdc0.html

OPEC upheaval delivers a broadside to major energy companies as oil prices plunge sharply | Fox Business

Plunging Crude Prices Hammer Energy Companies - ABC News

I will add this.Expect the United States to go into a recession Q1 of 2015.Our largest export(162 billion in 2013)was refined petroleum product.The oil price will shave a good deal off our GDP and hurt our already terrible trade imbalances.Add to that the amount of debt tied to fracking/shale oil companies and the reason for some of those companies losing 50%+ of their value in the last 48 hours becomes clear.Margin calls where happening all over the fracking world today,and will continue Monday I am sure.

Exxon,the largest company in the world lost 9% of its value in 48 hours,and is no longer the largest market cap.

I am also going to do something I should not,but the worst that can happen is I am wrong.

I am going to call the DOW 17,828.24 the record high(today's close).No QE,debts blowing up,congressional hearing on bank manipulation of physical commodities release today including oil with blame clearly placed by both Republicans and Democrats on the committee at the Federal Reserve(http://www.zerohedge.com/news/2014-...roleum-and-other-physical-markets-then-manipu ) and I just do not see much to justify the 25.1 PE.

11/28/2014

Side note.When I say no QE I am talking about QE3.QE 1.5,that is using funds from maturing MBS and Treasuries is still ongoing,and means the FED has not totally taken away the punch bowl.It is substantially less than QE3 though.

Last edited:

The Bubba Effect

Grandmaster

So . . . this means what for Joe Schmoe? What should a guy with a small nest egg do with his money?

That is the question.

All I have to do is wait for the market to crash, be perfect in calling the bottom and dump it all into some of the legit companies that catch part of the collective beatdown.

Easy Peasy

So . . . this means what for Joe Schmoe? What should a guy with a small nest egg do with his money?

If I were him, I would save aggressively. Hold the increase of my net worth (as investible or income-producing assets) above all other financial measures. Invest for the long term in a portfolio diversified across asset classes and global markets, in accordance with my personal tolerance for risk. Ignore the pundits, the talking heads, and the financial news. Stay the course.

Last edited:

Anyone used Fidelity your investments?

For example, a 401k rollover from former employer; what funds have you seen do the best? When do you change your allocations?

I'm just looking for some wisdom on how to do something other than letting it sit in the same thing and hope it doesn't take a beating.

For example, a 401k rollover from former employer; what funds have you seen do the best? When do you change your allocations?

I'm just looking for some wisdom on how to do something other than letting it sit in the same thing and hope it doesn't take a beating.

Anyone used Fidelity your investments?

For example, a 401k rollover from former employer; what funds have you seen do the best? When do you change your allocations?

I'm just looking for some wisdom on how to do something other than letting it sit in the same thing and hope it doesn't take a beating.

That is a question for a very different forum. Try some of these links:

Bogleheads Investing Advice and Info

Getting started - Bogleheads

Bogleheads ? Index page

And if you want to read from some people who've been very successful managing their finances, you can find them here:

Early Retirement & Financial Independence Community

That forum is clearly not all about finance, but you'll find most of them are pretty savy when it comes to money. Especially the ones who retired before 50 (sometimes significantly before 50).

That is a question for a very different forum. Try some of these links:

Bogleheads Investing Advice and Info

Getting started - Bogleheads

Bogleheads ? Index page

And if you want to read from some people who've been very successful managing their finances, you can find them here:

Early Retirement & Financial Independence Community

That forum is clearly not all about finance, but you'll find most of them are pretty savy when it comes to money. Especially the ones who retired before 50 (sometimes significantly before 50).

thanks Jackson

thanks Jackson

No problem. If you were interested in books, I'd say start with these:

A Random Walk Down Wall Street by Burton Malkiel

A Random Walk Down Wall Street: The Time-Tested Strategy for Successful Investing (Eleventh Edition): Burton G. Malkiel: 9780393246117: Amazon.com: Books

Four Pillars of Investing by William Bernstein

http://www.amazon.com/Four-Pillars-...513&sr=8-1&keywords=four+pillars+of+investing

Anything by John Bogle (Founder of Vanguard mutual fund company):

http://www.amazon.com/John-C.-Bogle/e/B001H6NWEM/ref=sr_tc_2_0?qid=1417232628&sr=8-2-ent

Some of the stuff by the Boglehead folks aren't bad, but usually somewhat general:

The Bogleheads' Guide to Investing: Taylor Larimore, Mel Lindauer, Michael LeBoeuf, John C. Bogle: 9781118921289: Amazon.com: Books

The Bogleheads' Guide to Retirement Planning: Taylor Larimore, Mel Lindauer, Richard A. Ferri, Laura F. Dogu, John C. Bogle: 9780470919019: Amazon.com: Books

I also found the Millionaire Next Door by Thomas Stanley to be a pretty good read. This is not about investing, but about the habits, ways, and lifestyles of average millionaires. However, the second book titled The Millionaire Mind was not as good. I picked it up at Half Priced Books and was glad I didn't pay full price.

The Millionaire Next Door: The Surprising Secrets of America's Wealthy: Thomas J. Stanley, William D. Danko: 9781589795471: Amazon.com: Books

If I were him, I would save aggressively. Hold the increase of my net worth (as investible or income-producing assets) above all other financial measures. Invest for the long term in a portfolio diversified across asset classes and global markets, in accordance with my personal tolerance for risk. Ignore the pundits, the talking heads, and the financial news. Stay the course.

Thanks, Jackson.

I've been literally scared of traditional investments such as mutual funds for a while now. Recently they're doing okay, but I can't shake how much my parents lost in 1999-2000 and then again in 2008. Emotionally it's heart breaking to see that kind of loss when someone did everything "right" and made big sacrifices to prepare for the future. On a practical level, I simply can't afford to lose any of what I have, so my tolerance for risk is very low. That is especially true since I'm getting such a late start on a "career" and I don't have that much time to stay the course and wait for improvements if things go bad.

Thanks, Jackson.

I've been literally scared of traditional investments such as mutual funds for a while now. Recently they're doing okay, but I can't shake how much my parents lost in 1999-2000 and then again in 2008. Emotionally it's heart breaking to see that kind of loss when someone did everything "right" and made big sacrifices to prepare for the future. On a practical level, I simply can't afford to lose any of what I have, so my tolerance for risk is very low. That is especially true since I'm getting such a late start on a "career" and I don't have that much time to stay the course and wait for improvements if things go bad.

What was lost in those two periods has been recovered, at least from a broad market perspective. Those who were diversified and stayed the course survived. Those who invested more in those down markets did even better.

Consider your time horizon is your likely life expectancy, not your expected retirement date. Unless you die shortly after retirement, you'll need to be invested to keep up with inflation and maintain a usable withdrawl rate. Choose an asset allocation with a volatility that allows you to sleep. Save as much as you can manage.

What was lost in those two periods has been recovered, at least from a broad market perspective. Those who were diversified and stayed the course survived. Those who invested more in those down markets did even better.

Consider your time horizon is your likely life expectancy, not your expected retirement date. Unless you die shortly after retirement, you'll need to be invested to keep up with inflation and maintain a usable withdrawl rate. Choose an asset allocation with a volatility that allows you to sleep. Save as much as you can manage.

Overall in terms of the markets, I can't argue with that. I can say with absolute certainty that my parents stayed the course, were well diversified, etc. but they did not recover. Yes, they "survived," but just barely. While their situation may be an exception, it is far more pertinent to us than the bigger picture that the markets made a comeback and most other people did okay over time.

I do save a much bigger percentage than average. I'd be in better shape if interest rates were allowed to go to reasonable levels and CDs and other fraidy cat investments could outpace the practical real world level of inflation.

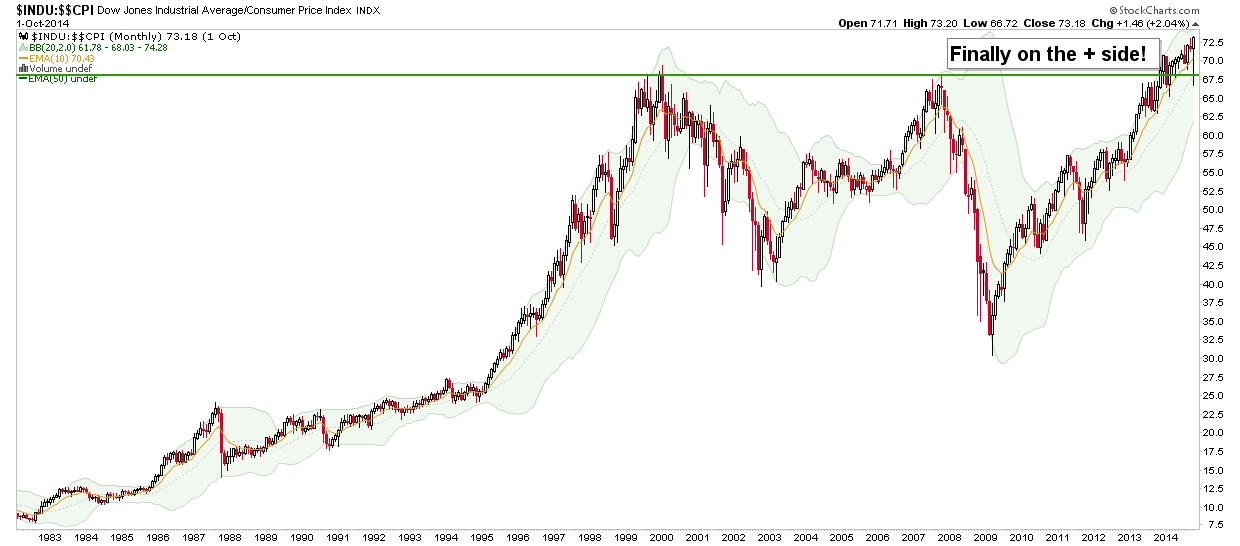

Your concerns are very justified. The stock market only reached positive returns since 2000 on an inflation-adjusted basis just recently. link

Inflation-adjusted returns (click image to expand):

Unfortunately, the stock market has been running through a series of bubbles with the dot-com bubble in 2000, the housing bubble in 2008, and a QE-driven bubble now. With the Fed holding bank-level interest rates at right around 0% (other interest rates are based on this), savings, CD and "safe" bond returns are negative vs. inflation. Basically, paper assets just aren't a great place to try and maintain/build wealth.

Inflation-adjusted returns (click image to expand):

Unfortunately, the stock market has been running through a series of bubbles with the dot-com bubble in 2000, the housing bubble in 2008, and a QE-driven bubble now. With the Fed holding bank-level interest rates at right around 0% (other interest rates are based on this), savings, CD and "safe" bond returns are negative vs. inflation. Basically, paper assets just aren't a great place to try and maintain/build wealth.

Last edited:

Site Supporter

Staff online

-

KellyinAvonBlue-ID Mafia Consigliere

KellyinAvonBlue-ID Mafia Consigliere

Members online

- MeltonLaw

- usmcdjb

- WebSnyper

- grunt soldier

- actaeon277

- Creedmoor

- JimH

- KellyinAvon

- INgunowner

- racegunz

- ductape

- brizzad

- Lilboog82

- r3126

- buckwacker

- Roadman

- red_zr24x4

- Glock22

- Angrysauce

- mike trible

- SmileDocHill

- slipnotz

- boostjunki

- PowderApe

- phylodog

- klausm

- Farmerjon

- soupy

- Joniki

- HKFaninCarmel

- Goodcat

- knutty

- ChooterMcGavin1973

- traderjoe

- KJQ6945

- AmericanBob

- GSPBirdDog

- jbm1521

- 4sarge

- Wfulton

- mhs

- 55fairlane

- pokersamurai

- ComeJesuscome

- XDdreams

- Gravyman

- freekforge

- peterock

- jtmiller951

- skulhedface

Total: 10,042 (members: 281, guests: 9,761)